Stamp duty is a tax that's charged when you buy a property in the UK, but you'll only need to pay it if the price of that property reaches a certain threshold. Our guide below shows you just how much you'll need to pay. Read the full guide for exactly how stamp duty works in different parts of the UK and when you need to pay it by.

What is stamp duty?

When you buy property or land, you usually pay tax on it. This is called stamp duty land tax in England and Northern Ireland, land and building transaction tax in Scotland and land transaction tax in Wales

In 2023, the average stamp duty bill for homebuyers in England and Northern Ireland was around £10,000, amounting to £11.5 billion spent on stamp duty overall, according to Coventry Building Society.

Below we explain exactly how stamp duty works –

Stamp duty rates

Here's how the thresholds and rates differ across the UK nations.

England and Northern Ireland

In England and Northern Ireland, no stamp duty is due on the first £250,000 of a main residential property – though that threshold is £425,000 if you’re a first-time buyer.

Here are the stamp duty rates you'll pay on a main residential property:

Some people buying a property in England and Northern Ireland have to pay a higher rate of stamp duty because they are considered 'non-residents' of the UK.

Non-resident status will apply if you do not spend at least 183 days anywhere in the UK (which can include Scotland, Wales) during the 12 months prior to purchasing the property. Do note that the rules are more complex if you're married.

Where you have to pay the non-resident rate of stamp duty, it'll be equivalent to an extra two percentage points on top of normal stamp duty rates. For example, a non-resident first-time buyer purchasing a property for £500,000 would pay:

- 2% stamp duty (rather than 0%) on the property price up to £425,000.

- 7% stamp duty (rather than 5%) on the property price between £425,000 and £500,000.

For more information on how non-resident status works in relation to stamp duty, see the Gov.uk website.

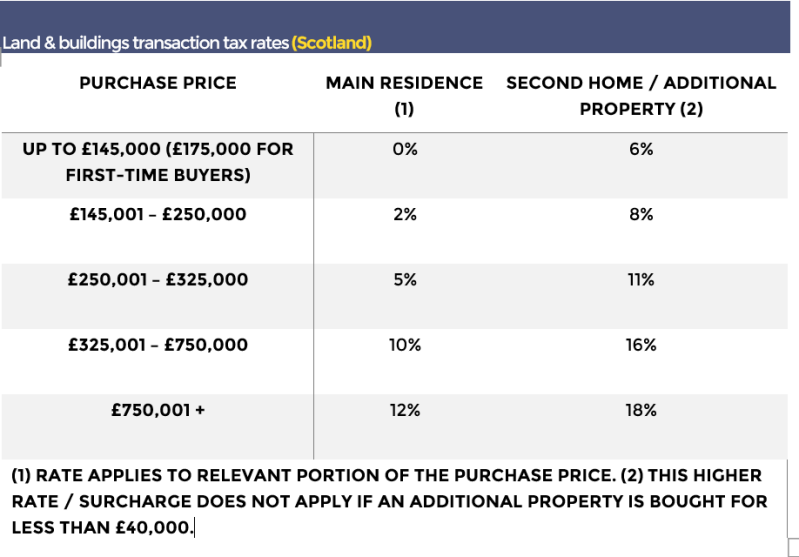

Scotland

The main difference between stamp duty in Scotland and England / Northern Ireland is the thresholds and rates that are used – though the Scottish system does have extra relief for first-time buyers, like in England and Northern Ireland.

Here are the stamp duty rates you'll pay on a main residential property:

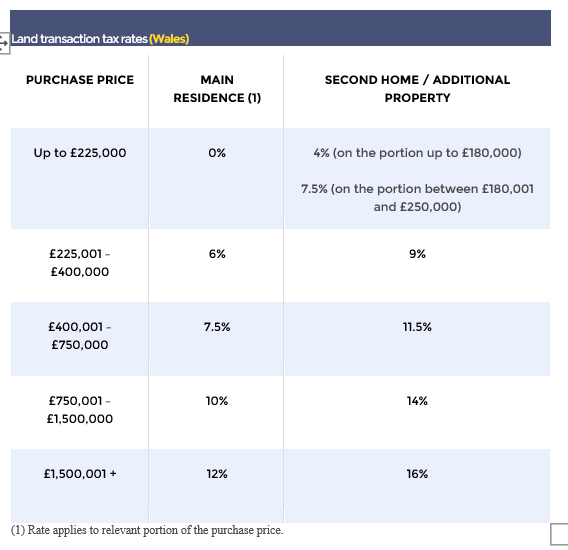

Wales

In Wales, the stamp duty thresholds and rates are different to those in England, Northern Ireland and Scotland – plus there is no extra relief for first-time buyers.

Here are the rates you'll need to pay:

Stamp duty for first-time buyers

It can be confusing to work out exactly how much stamp duty a first-time buyer needs to pay with the extra 'relief' available in England, Northern Ireland and Scotland.

For the purposes of stamp duty, you WON'T be considered a first-time buyer if you've ever owned, or part-owned, a property in the UK or abroad. This includes if you've ever inherited a property – even if you sold it straightaway and never lived in it.

England and Northern Ireland

First-time buyers don't pay stamp duty on the first £425,000 of a main residential property (provided the property you're buying costs £625,000 or less).

Wales

First-time buyers pay don't pay land transaction tax on the first £225,000 of a property (this applies to all buyers of a main residential property)

Scotland

First-time buyers don't pay land and buildings transaction tax on the first £175,000 of a property.

Buy-to-let and second home stamp duty

Where you buy a property in addition to one you already own – for example a second home (or third, fourth, etc) – you'll need to pay a higher rate of stamp duty:

- In England and Northern Ireland the higher rate of stamp duty is equivalent to an extra three percentage points on top of standard rates.

For example, if you were buying a second home for £300,000, you would pay £11,500 in stamp duty, whereas if it was your only property (and you weren't a first-time buyer), you'd only pay £2,500. - In Scotland it's equivalent to an extra six percentage points.

So, on a second property worth £300,000, you'd pay £22,600. That compares to £4,600 if the house you were buying was your only property (and you weren't a first-time buyer). - In Wales it's equivalent to an extra four percentage points.

So, on a second property worth £300,000, you'd pay £16,950 in stamp duty. That compares to £4,500 if the house you were buying was your only property.

This higher rate also applies if you're buying an additional property with the intention of renting it out (known as buy-to-let). However, if you're a first-time buyer intending to rent your property out as a buy-to-let then you won't need to pay the higher rate – though you won't qualify for first-time buyer stamp duty relief either.

When must I pay stamp duty?

In England or Northern Ireland, you have 14 days from the date of completion/date of entry (when all the contracts are signed and dated, and you get the keys – read our Buying a home guide for a full timeline) to pay any stamp duty due.

In Scotland and Wales, you have 30 days.

Take longer, and you could face a fine and possibly interest on top, so don't.

In reality, your solicitor will probably sort this out and push you to pay the bill straightaway – in fact, most tend to want their cash before completing the property purchase for you, just in case you then can't or don't pay them.

However, it's legally your responsibility to ensure your stamp duty/transaction tax is paid. If you are doing this yourself, click the questions to see the process.

Adding stamp duty to a mortgage

The simple answer here is that it's best that you don't, but many people find that they have to.

To add the cost of stamp duty to your loan means a bigger mortgage debt. So, in England and Northern Ireland, say you needed a £180,000 mortgage to purchase a house costing £300,000 but wanted to add the stamp duty, you'd need to request borrowing of £182,500 – then use your 'extra' deposit money to pay the stamp duty.

There are two main things to consider here. Firstly, as mortgages tend to be taken out over a long term (25 years or more), that's normally how long the stamp duty borrowing will last too. Over a 25-year term at a rate of 5%, that extra £2,500 borrowing will cost about £6,000 in interest, so it's vital to be aware of the cost.

Secondly, this could affect your loan-to-value ratio (LTV) – the measure of how much of a property's value you are borrowing. The most competitive deals require a maximum LTV of 60% – yet in the example above, adding the stamp duty would push you from 60% to almost 62%, so be careful – speak to us to see if it's the right decision. ( Book a Consultation) Follow us for more tips on Insta: solapemortgagesandprotection

Add comment

Comments